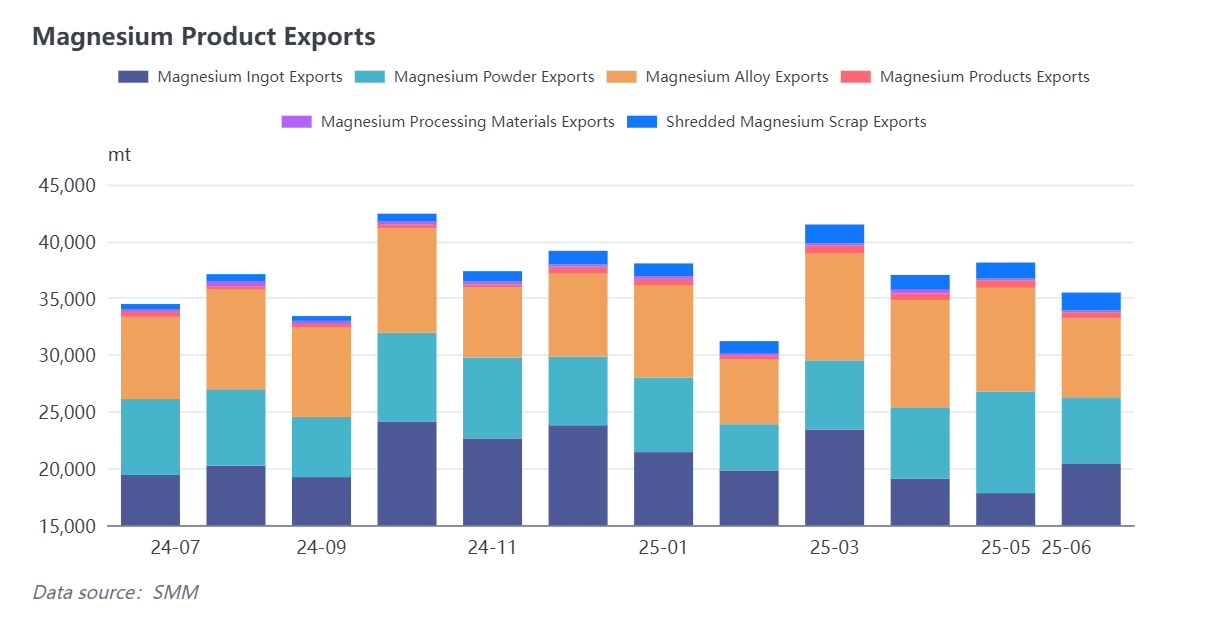

From the overall performance of magnesium product exports in June, the cumulative export volume continued to show a downward trend. Specifically, after a concentrated export procurement period in May, magnesium powder and magnesium alloys have now entered the traditional off-season, with exports of both products showing varying degrees of decline. Meanwhile, magnesium ingots saw a slight increase in exports month-on-month due to price adjustments and the seasonal procurement cycle of enterprises. However, from the overall export order situation, major export regions remain cautious in their procurement, with weak end-use demand being particularly evident.

From the overall performance of magnesium product exports in June, the cumulative export volume continued to show a downward trend. Specifically, after a concentrated export procurement period in May, magnesium powder and magnesium alloys have now entered the traditional off-season, with exports of both products showing varying degrees of decline. Meanwhile, magnesium ingots saw a slight increase in exports month-on-month due to price adjustments and the seasonal procurement cycle of enterprises. However, from the overall export order situation, major export regions remain cautious in their procurement, with weak end-use demand being particularly evident.

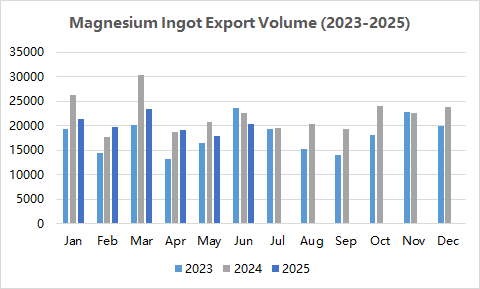

According to the latest customs statistics, the total export volume of magnesium ingots from China reached 20,393 tonnes in June 2025, representing a month-on-month increase of 14.38% compared to the previous month. However, this figure still represents a year-on-year decrease of 9.63% compared to the same period in the previous year. Looking at the cumulative export data for the first half of the year, the total cumulative export volume of magnesium ingots from January to June was 122,021 tonnes, a decrease of 10.64% compared to the same period in 2024. This data clearly reflects the overall trend of continued contraction in the demand for magnesium ingot exports.

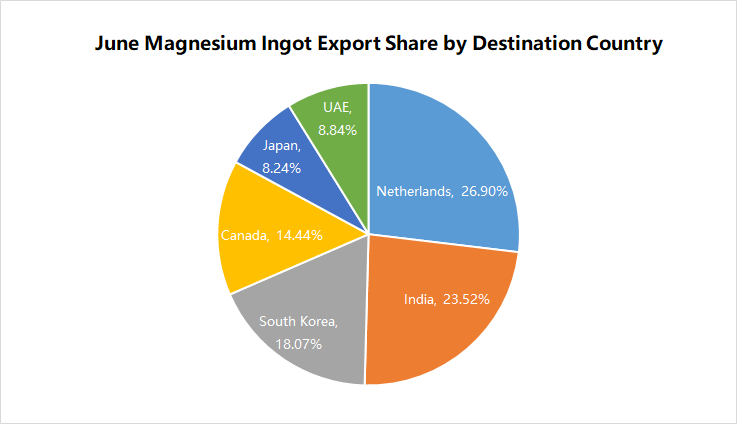

From the distribution of magnesium ingot export destinations in June, as the primary transshipment port for magnesium ingot imports in Europe, the Netherlands continues to hold the position of the largest export destination for Chinese magnesium ingots. However, it is worth noting that exports to the Netherlands have been steadily declining, with June exports totaling only 3,110 tonnes, representing a significant year-on-year decline of 55.69%. Meanwhile, the Indian market has performed strongly, with imports reaching 2,719 tonnes in June, a month-on-month increase of 29.47%. Against the backdrop of continued weak demand in the European market, India is gradually reshaping the traditional export landscape for China's magnesium ingots. Additionally, overall demand in the Asian and North American markets remains stable, with procurement activity in the Japanese and South Korean markets showing some improvement.

Although June is traditionally a peak procurement season, the overall export performance of the magnesium industry still fell short of expectations. The current market exhibits typical characteristics of both weak supply and demand: on the one hand, domestic magnesium plants have generally implemented production cuts, leading to a sustained contraction in supply; on the other hand, overseas market demand is constrained by multiple factors, including slow progress in the promotion of magnesium alloy application technologies, heightened volatility in international shipping costs, and trade policy uncertainties stemming from geopolitical factors. In this complex environment, downstream customers have generally adopted more conservative procurement strategies, strictly controlling procurement pace and inventory levels.

In addition, Announcement No. 17 of 2025 issued by the State Administration of Taxation of China on 7 July strengthened the supervision of corporate income tax for export enterprises, requiring that actual cargo owner information be disclosed for agency export business. This new regulation will take effect on 1 October 2025, effectively standardising the export order of the magnesium industry, curbing irregular operations such as ‘purchasing customs declarations for exports,’ and promoting the return of the industry to the essence of genuine trade. SMM will continue to monitor the impact of policy implementation on magnesium product export prices and trade patterns, and provide timely professional analysis.